Management Control ensures the human physical and technological resources are allocated and utilised to achieve the overall purpose of the organisation. The feedback control is about monitoring the outputs desired against outputs achieved. There are many ways of management control which include feedback, feedforward, bench-marking and auditing. Most of these are usually employed by progressive organisation.

Management Control systems

Management Control systems

Control

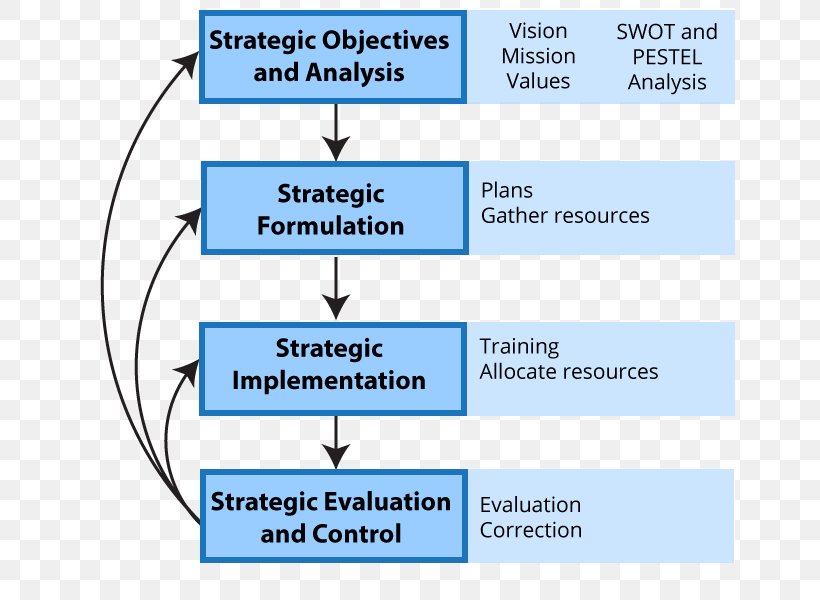

Control is a process whereby management ensures that the organisation is achieving the desired objectives. It is a set of organised (adaptive) actions directed towards achieving specific goals in the face of constraints (Wilson and Gilligan, 1997). The existence of a control process enables management to know from time to time where the organisation stands in relation to the organisation's goals. This implies that progress should be observed, measured and redirected if there are discrepancies between the actual and the desired positions. Control and planning are complementary and each should logically pre-suppose the existence of the other. Maciariello (1984) gives the following definition of management control (MC) and management control system (MCS).

Management control is the process of ensuring that the human, physical and technological resources are allocated so as to achieve the overall purposes of an organisation. An MCS attempts to bring unity of purpose to the diverse efforts of a multitude of organisation's and the managers towards its objectives and goals. An MCS consist of a structure and a process.

However, the interpersonal nature of control within an organisations needs to be recognised in order to relate to motivation, goal congruence and the reward system as indicated by Hosted (1968) who states that “control within an organisation system is the process by which one element (person, group, norm, machine or institution) intentionally affects the action of other elements”.

Strategy is seen as being related to control. However, it can be treated separately. This is because it is possible for an enterprise with good strategies to fail, when the control system is poor and vice versa. In general, the better the formulation of a strategy, the greater will be the number of feasible control alternatives and the easier their implementation is likely to be, according to Wilson and Gilligan.

Anthony (1988) refers both to the hanks between control and strategic implementation on one hand and the interaction among the individuals on the other. He says that “control is used in the sense of assuring implementation of strategies. The management control functions include making the plans that are necessary to assure that strategies are implemented.

Management control is the process by which managers influence other members of the organisation to implement the organisation's strategies. There are different ways by which an organisation carries out its management control. They do this by, feed forward, auditing, budgeting, feedback and bench-marking systems. These methods shall be considered in brief.

Feed Forward Control

This is defined as “a measurement and prediction system which assesses the system and predicts the out put of the system at some future date” Bhaskar and Housden (1985). This differs from a feedback system in that it seeks to anticipate and thereby to avoid deviations between actual and desired outcomes.

According to Costing (1982), the components of feed forward control system are:

- An operating process which converts an input to output.

- A characteristic of the process which is the subject of the control.

- A measurement system which assesses the state of the process

and its input and attempts to predict its output.

- A set of standards and or criteria by which the predicted state of the process can be evaluated.

- A regulator, which compares the predictions of process outputs to the standards and which takes corrective action where there is likely to be a deviation.

For the effectiveness of feed forward system, it must be based on a reasonable predictable relationship between inputs and outputs, i.e. there must be an adequate degree of understanding of the way in which the organisation functions.

Audit

This is an approach towards assessing marketing effectiveness Kotler (1984) offer the view that auditing is the ultimate control measure. It evaluates performance in terms of input used, output generated and the

assumptions underlying the marketing strategies used. The ranges of possible audits include:

(i) self audit

(ii) audit from across, i.e., by colleagues in another function

(iii) audit from above, by the manager or superior company audit office

(iv) company task-force audit, i.e. a team set up specifically to conduct the audit,

(v) outside auditors.

It is usually better to have a combination of these methods.

Budgeting

A budget is a quantitative plan of action that aides in the co-ordination and control of acquisition, allocation and utilisation of resources over a given period of time. Budgeting is also known as profit planning. It is the widest ranging control technique. It covers the entire organisation rather than to a section of it. Typically, budget is compiled on an annual basis. The time span can however, be broken into half-a-year, quarterly, monthly and even weekly. Regardless of whether the budget is a long-term or short-term one, continuous or periodic budget, the fundamental requirements that should be met include the following:

- established objectives

- top management support and sponsorship

iii. a knowledge of cost behaviour

- flexibility

- a specific time period

- adequate system support

vii. effective organisational structure

viii. sufficient level of education in budgetary practice.

Feedback Control

Feedback control is about monitoring of outputs achieved against desired outputs from time to time and to take whatever corrective action is necessary if a deviation exist. This is referred to as the feedback control. The feedback control system is depicted in Fig. 9.

The feedback control entails honking outputs with letter elements within the system. It may be termed close-loop control system.

Feedback control should ensure self-regulation in the face of changing circumstances once the control system has been designed and installed. The importance of feedback control is found in homeostasis which defines the process whereby key variables are maintained in a state of equilibrium even when there are environmental disturbances.

For example, if a company plans to sell 100,000 strategic management books, in the next 12 months and by the end of the third month, the pattern of demand falls to 80,000 books due to the launch by another company of a good strategic management book which is a competing book. After another three months, the competitor puts up the price of his own book while the original company holds its own price constant. By this technique the demand may increase to 150,000 units.

The feedback signals should ensure that the company is aware through monthly reports, may be of the archival sales versus planned sales. So, the launch of the strategic management book by a competitor would be identified as the reason why sales levels were below expectations in the early period of the first three months.

|

| A Feedback Control System |

In response to the derivations between actual and desired results (feedback) an explanation must be found and actions taken to make corrections. Such corrective measures may include amending

production plans to print fewer (or more) books, allowing inventory level to fall (or rise) to meet the new demand pattern and modification of the promotional plans to counter competitive activities. These could all come from a feedback control system.

However, if the derivations (variances) from the feedback are minor it may be possible for the process to absorb them without any modification. An inventory control system could just be designed to accommodate such minor variations between the expected and the actual levels of demand with buffer stocks being prepared for the purpose.

In the case of extreme situations in which the stock has to change from 100,000 to 80,000 and 150,000 units, the inputs have to be amended deliberately as soon as the cause of the variations has been identified. There is usually a cost associated with variance, which tend to be proportional to the length of time it takes to identify and correct the variations. Cushing (1982) suggests some principles for the proper functioning of a feedback control system which include:

- The benefits from the system should be at least as great as the costs of developing, installing and operating it. It is often difficult to specify precisely the benefits (except in situations such as better customer service, increased efficiency) or the costs of relating to different system designs, but estimations of these could be made.

- Variance, once measured should be reported quickly to facilitate prompt control action.

iii. Feedback reports should be simple, easy to understand and highlight the significant factors requiring managerial attention.

- Feedback control systems should be integrated with the organisational structure of which they are part.

The boundaries of each process are subject to control and should be within a given manager's span of control.

Bench-Marking Control

The bench-marking control system is an analytical process through which an enterprise's performance can be compared with that of its competitors. It is used by organisations such as Xerox and Ford in order to be able to evaluate the following:

- Identify the key performance measures for each business function.

- Measure one"s own performance and that of the competitors.

iii. Identify areas of competitive advantage or disadvantage by comparing performance levels.

- Design and implement plans to improve one"s own performance on key issues relative to competitors.

Bench-marking is applicable in other functional areas with the potential to help change the corporate culture, if properly communicated throughout the organisation. In the case of bench-marking products or services offered by customers but not by itself, an enterprise"s senior manager can gain insights to guide its decisions by keeping abreast of new developments. In this way, it will be easier to assess how to respond.

When considering how to take corrective action, it is important to make an assessment of the probable response of competitors to any action that might be taken. This is a vital aspect of strategic behaviour. It is expected that the identities of the competitors are known (both actual and potential), and profiled. The possible responses from them can then be explored, taking into account conjectures regarding the beliefs that the competitors have of one"s own enterprise including its resources, capabilities and strategies.

Process of Making Corrective Adjustment

There is no one strategic plan or strategic scheme for implementation that can foresee all the events and problems that may arise in future.

Process of Making Corrective Adjustments

Process of Making Corrective Adjustments

Adjustment making or “mid-course” corrections are normal and a necessary part of strategic management.

When there is a need to react or respond to a new condition involving the strategy or strategy implementation, the process of what to do has to be evaluated. This evaluation must consider whether the action should be immediate or whether the time permits a more deliberate response. In cases where time permits a full-fledged evaluation, strategy managers prefer a process of solidifying commitment to a response. This approach includes these:

- To stay flexible and keep a number of options open.

- To ask a lot of questions.

- To gain in-depth information from specialists.

- To encourage subordinates to participate in developing alternatives and proposing solutions.

- To get the reactions of many people to proposed solutions as a test of their potential and political acceptability.

- To seek to build commitment to a response by gradually moving towards a consensus solutions.

The overriding principle seems to be to make a final decision as late as possible so as to make as much information to bear as is needed; or let the situation clarify enough to know what to do or allow the various political constituencies and power basis within the organisation to move towards a consensus solution

Corrective adjustment to strategy need not be just reactive. A proactive adjustment constitutes a second approach to improving strategy or its implementation. The distinctive feature of a proactive posture is that adjusting actions arise out of management's own drives and initiatives for better performance as opposed to forced reactions.

Successful strategy managers have been known and observed to employ a variety of proactive tactics.

The key feature of strategic management is that the job of formulating and implementing a strategy is not one of steering a clear-cut, linear course of carrying out the original strategy intact according to some perceived and highly detailed implementation plan. Rather, it is one of operatively (1) adapting and reshaping strategy to unfolding events (2) employing analytical-behavioural-political techniques to bring internal activities and attitudes into alignment with strategy.

The process is interactive, looping and re-cycling to fine-tune and adjust in a congruously evolving process where the conceptually separate acts of strategy formulation and strategy implementation blur and joint together. Corrective active action comes after plan implementation, performance monitoring and analysis of significant valances. For example, how should an enterprise respond to changes in the environment? Usually, there are many ways. However, Barrett (1986) points out two opposing possibilities. The two approaches are as follows:

Deterministic Approach

In this approach, it is felt that the enterprise's environment determines its actions, its strategies and structure. The idea of adaptation to environmental change is hereby taken to an extreme. It is a known fact that changes in the environment, either in the form of opportunities or threats, will result in a competitive strategy. The implementation of these changes may bring about changes in the organisation's structure.

Strategic Approach

Contrary to the deterministic approach, strategic approach sees the environment as constraining the enterprise's freedom of action rather than determining the action. It therefore, concentrates more on the enterprise'^ strengths and weaknesses and its ability to influence its environment rather than simply being influences by the environment. A good example is the strategy of raising barriers to entry which modifies the environment against the interests of potential competitors.

In these two approaches, management intelligence has a lot of roles to play by identifying environmental changes as a basis for reactive or proactive responses.

Strategy implementation and Control

The successful implementation of a strategy is not easy. And if implementation is left to compete with internal pressures of coping with crises, reacting to competitor's action, company policies and personal career needs, it is most likely to be disrupted.

Strategy implementation and Control

Strategy implementation and Control

Plan implementation poses a fundamental dilemma. This is because, to be effective, forces leading to organisational integration must be reconciled with forces leading to organisational segmentation. There are two opposing forces. To achieve a balance therefore, the following have to be considered.

- The messages of the plan should be communicated so that there will be a proper understanding of the plan.

- There should be a clear recognition of what the plan says, so that the all those who have a role to play in the plan implementation are aware of their roles.

- There should be a consensus about the wisdom of pursuing the plan in order to secure commitment to its accomplishment.

Strategy Implementation and Information Control

The effectiveness of a manager on his job will depend on how much, how relevant and how good his information is, and how well he interprets and acts on such information. Usually, the complaint is that the information is too late, is of the wrong type, unverified or even suppressed. So, for information to be of value, it must be clear, detailed, timely, accurate and complete and must not contain vague figures thrown out by an unplanned system. The information must be explicit.

0 Comments