n the previous article, we discussed the projected cash flow statement. There, we discussed inflows and outflows (outgoings) of a firm or project. We also discussed the structure of the projected cash flow statement and went a step further to provide an example of a projected cash flow statement. In this post, we shall discuss the projected balance sheet.

Meaning of a Balance Sheet

Before we delve into the projected balance sheet proper, it is very important for us to first understand what a balance sheet is. The balance sheet or the statement of financial position is one of the most important financial statements. It shows the financial condition or better still, the statement of affairs of a firm or business. We Will therefore, define a projected balance sheet as a forecast of a future balance sheet as at a future date.

Components of the Balance Sheet

The balance sheet has two main sides namely:

Assets

When we are talking of assets generally, we are talking about the valuable possessions owned by the firm, valued in monetary terms. They will include land and buildings, stock of goods, raw materials, cash, vehicles and other valuables.

But generally we can classify assets under the following headings:

Lets us now discuss each of them:

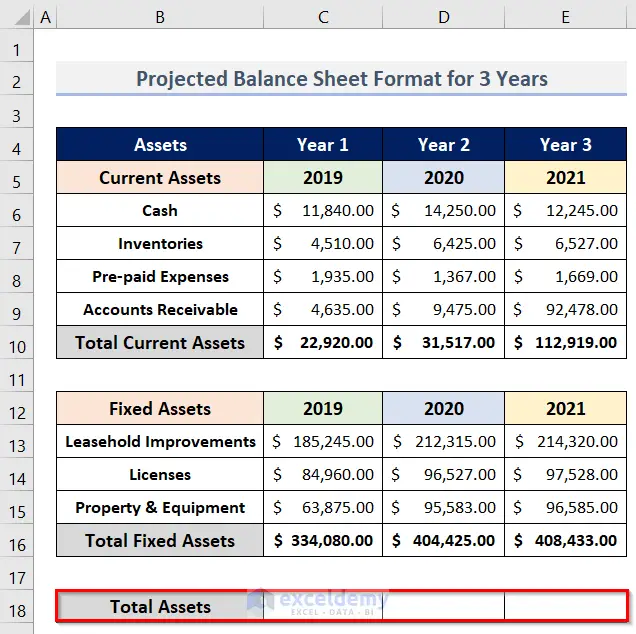

Current Assets

The current assets of a firm or business are those assets which are held in the form of cash or expected to be converted into cash in a period or within the accounting period of the firm. In actual practice, the accounting period is usually of one-year duration. The current assets of the firm will include the following:

Let us start with cash which is one of the most liquid current assets. Cash will mean cash on hand or cash in the bank.

Another current asset which is important is book debts (debtors). Book debts are sometimes called account receivables. These are amounts due from debtors to whom goods have been sold or service rendered. Some of the book debts may be realised by the firm. If they are not realized they turn into what is called bad debts and may be written off later.

Prepaid expenses are also current assets. They are expenses of future periods that are paid in advance. An example of prepaid expenses is rent which may be payable in advance by a firm. For example in January 2007, a firm may pay rent for its office for January 2007 to December, 2007. If in April, 2007, the financial year of the firm ends, it will regard the portion of rent paid from May 2007 to December, 2007 as a prepaid expense which invariably is a current asset.

Stock (inventory) is another current asset and includes raw material, work in process and finished goods. The raw materials and work in process are required for maintenance of the production function of the firm.

Finished goods usually will be already packed and kept ready for purchase by customers of the business. Marketable securities are the firm’s short term investment in shares, bonds and other securities. The securities are usually marketable and can be converted into cash in a very short time.

Investments

Investments represent the firm’s investments in shares, debentures and bonds of either firms or the government. By their nature, the investments are long term. It is important to note that the investments yield income to the firm.

Fixed Assets

Fixed assets are long-term assets held for periods longer than one year. They are usually held for use in the firm’s business. Fixed assets include land, buildings, machinery and equipment, vehicles, etc.

We have briefly seen what the assets are. We shall now move over and discuss liabilities.

Liabilities

When we talk of liabilities, we mean the debts that are payable by the firm or business to creditors. They may represent various obligations due to various third parties arising from various business transactions.

Examples of liabilities include creditors, accounts payable, taxes payable, bonds, debentures, etc. But generally, liabilities are divided into two broad groups namely:

We shall discuss each of the groups

Current Liabilities

Current Liabilities are those debts that are payable in a short period usually within a year. One of the major current liabilities is the bank overdraft. Most banks grant their customers overdraft which are repayable within a period of one year. The other type of current liability includes provisions for taxes and dividends. These are liabilities that will mature within one year.

Another type of liability is expenses payable. The firm may expenses to public power supply organisation or have rents to be paid.

Long Term Liabilities

Long-term liabilities are the obligations which are payable in a period of time greater than a year. One of the long term liabilities of a firm is term loan. The firm may borrow money from a bank that will be repayable over a period preceding one year. Such a borrowing or loan is regarded as long-term liability. Also, when a firm needs to raise a large sum of money, it debentures. A debenture is an obligation on the part of a firm to pay interest and principal under the terms of the debenture.

However one of the most stable types of long term liability is owners’ equity. Owner’s equity represents the owners’ interest in the firm. In practical terms, the total assets of a firm less the liabilities realized on the interest. The owners interest in the firm consist of

• Retained earnings (undistributed profits).

Construction of the Projected Balance Sheet

In the earlier sections of this unit, we have discussed the balance sheet generally. That was from a historical perspective. We shall now discuss the construction of a projected balance sheet.

The following steps are recommended:

• Start from the determination of sales revenue.

• Compute cost of goods sold (COGS)

• Compute admin expenses, general and selling expenses.

• Bring forward sundry income and expenses and generate the projected income statement.

• Determine taxation, dividends and retained earnings.

Table 36: A Projected Balance Sheet

Projected Balance Sheet (N)

| As at | Year 1 |

| Assets Employed | |

| Fixed assets | 66,629,024 |

| Preliminaiy expenses | 33,140 |

| Total | 66,662,164 |

| Current Assets | |

| Stock-in-trade | 12,000,000 |

| Raw materials | 12,000,000 |

| Debtors and prepayment | 1,000,000 |

| Cash and bank balance | 2,623,497 |

| Total Current Assets | 27,623,497 |

| Current Liabilities | |

| Creditors and accruals | 2,000,000 |

| Tax provisions | 10,247,185 |

| Total current liabilities | 12,247,185 |

| NET CURRENT ASSETS | 15,376,312 |

| Total Assets | 82,038,476 |

Record leases if any and project for the future amortisations.

Bring forward other sundry liabilities,

Estimate taxation based on the projected income statement and forecast the future trend.

From the net profit estimate amount going to dividends and retained earnings.

Record retained earnings. Record paid up capital. Fine tune grey areas.

Total the liabilities to agree with total assets.

CONCLUSION

We have discussed the projected balance sheet. We first discussed assets generally and then went ahead to discuss liabilities. We discussed the construction of the projected balance sheet and provided a checklist for the projection for both assets and liabilities.

We have treated the projected balance sheet. The projected balance sheet as we discussed is a forecast o

ASSIGNMENT QUESTIONS

1.

Who do you think are the users of the information in a

projected balance sheet?

2.

Why do they need the information contained in it?

REFERENCES AND

FURTHER READINGS

0 Comments